Recent Blog Posts

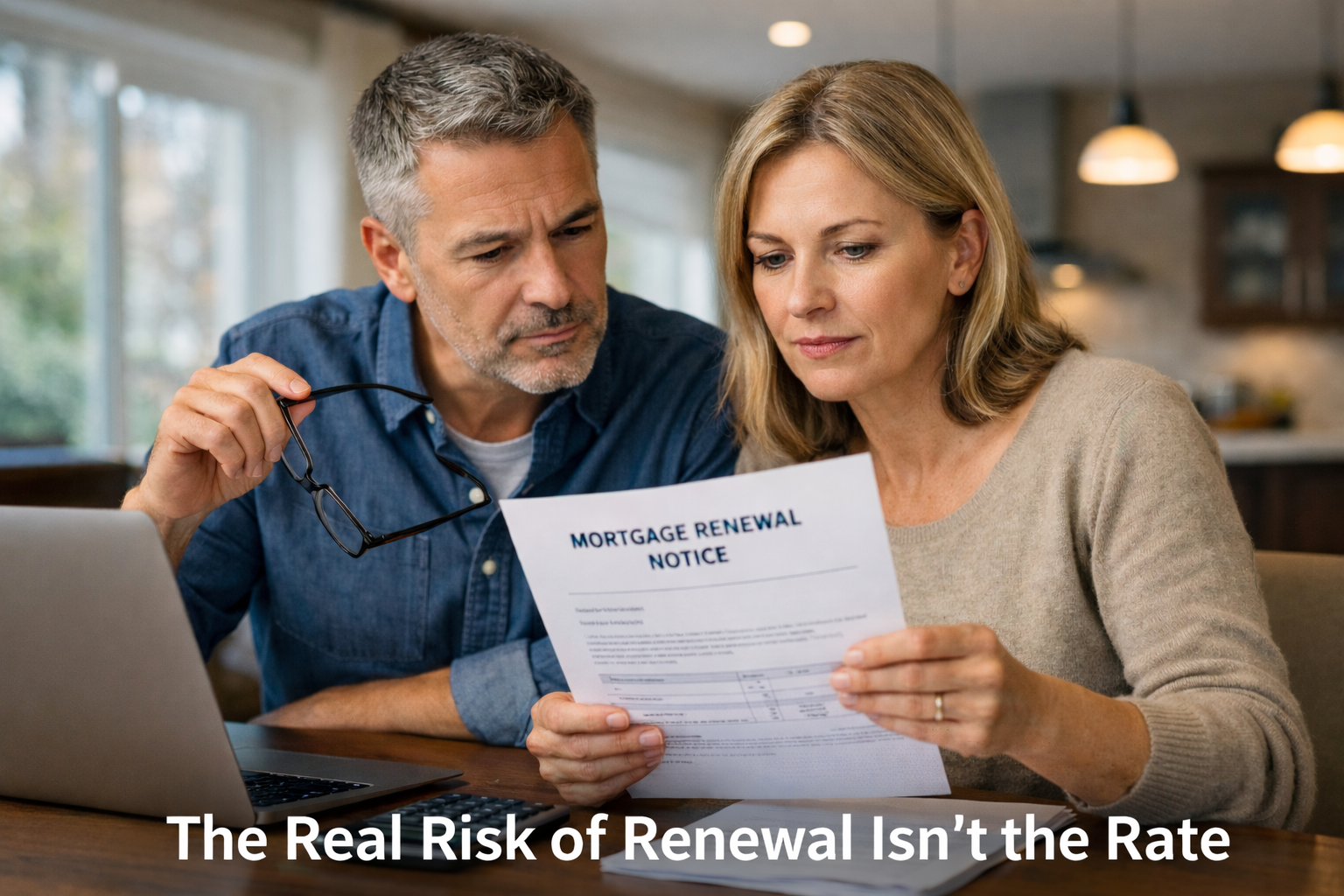

The Real Risk of Renewal Isn’t the Rate

Are Mortgage Rates Going to Drop in 2025? How U.S. Tariffs Could Impact You

With all the uncertainty surrounding Canada’s proposed capital gains tax changes, many property owners are asking, "Do I have to pay capital gains if I sell my house?" or "Should I sell my investment property before the tax rules change?" In June 2024 , the federal government proposed increasing the capital gains inclusion rate —the portion of capital gains that is taxable. This change could significantly impact investors and property owners selling secondary residences, rental properties, or cottages. But here’s the challenge: the rules haven’t been finalized yet. As Jamie Golombek explains in a recent Financial Post article, “ Uncertainty remains as to what the final capital gains tax rules will look like, or even if they will be implemented at all. ” Despite this uncertainty, the Canada Revenue Agency (CRA) has announced it will proceed with collecting taxes based on the proposed higher inclusion rate until a final decision is made. This means that even if you sell now, you could still face a larger tax bill. If the rules are later changed or rejected, the CRA may adjust tax filings—but in the meantime, selling could cost you more than you expect. The good news? Selling isn’t your only option. If you need access to cash or want to better manage your finances, refinancing or exploring alternative lending solutions could provide the flexibility you need—without triggering a large tax bill. Ways to Access Cash Without Immediately Selling If you need funds but aren’t sure whether selling is the best choice, here are some flexible ways to access cash while holding onto your property: 1. Refinancing Your Mortgage ● Access tax-free cash by using your home equity. ● Adjust your mortgage terms to fit your financial needs. ● Keep your property and continue building long-term wealth. 2. Alternative and Private Lenders ● Flexible lending options with easier qualification. ● Quick access to funds without selling your property. ● Short-term solutions to manage cash flow. 3. Reverse Mortgage (For Canadians 55+) ● Access tax-free equity with no monthly payments. ● Stay in your home while improving cash flow. ● Ideal for retirees on fixed incomes. 4. No-Payment Loan Options ● Interest-only or deferred payment loans. ● Manage expenses without immediate financial pressure. ● A flexible option to bridge financial gaps. Comparing Your Options: Sell or Keep Your Property? It’s important to weigh the pros and cons before making a decision. Here’s a simple comparison of selling versus other financing strategies:

When it comes to financing a home, amortization is a key term mortgage brokers often discuss. While shorter amortization periods are common in Canada, the concept of a 30-year amortization has gained traction among some buyers and brokers.

Moving to a new country is a big step, and finding a place to call your own can make settling in even more rewarding. For newcomers to Canada, the journey of purchasing a home can feel both exciting and overwhelming. This guide is here to help you navigate the process of buying a home in Canada, providing a clear roadmap and essential tips to make your homeownership dreams a reality.

2025 Reality Check: It’s not good. The Canadian real estate market is on the cusp of a significant shift. As we approach 2025, homeowners, especially investors and those with second homes purchased during the COVID-19 pandemic, face a challenging reality. Rising interest rates are set to dramatically increase mortgage payments, potentially making those once-affordable properties a financial burden.

As we navigate through 2024, the Canadian mortgage and real estate market faces a dynamic landscape marked by rising interest rates. This trend, driven by the Bank of Canada's efforts to curb inflation, has significant implications for homebuyers, homeowners, and real estate professionals. Understanding these changes is crucial for making informed decisions in this evolving market.

What does financial freedom mean to you? It's a question that might elicit a wide range of responses, and that's the beauty of it – financial freedom is a deeply personal concept.

When it comes to finding your perfect home, there are so many more options for potential homeowners! From a single-family dwelling to a townhouse to a modular home, the choices are seemingly endless. But, before you start widening your search, let’s take a look at what makes these home types different - and which one is perfect for you!

While home inspections might not be the most exciting part of your home buying journey, they are extremely important and can save you money and a major headache in the long run.