Should You Renew Your Current Mortgage?

Mortgage renewals with the same lender are popular because they are more straightforward. But does that mean you just sign on the dotted line? Here we try to elaborate on why you should change your lender.

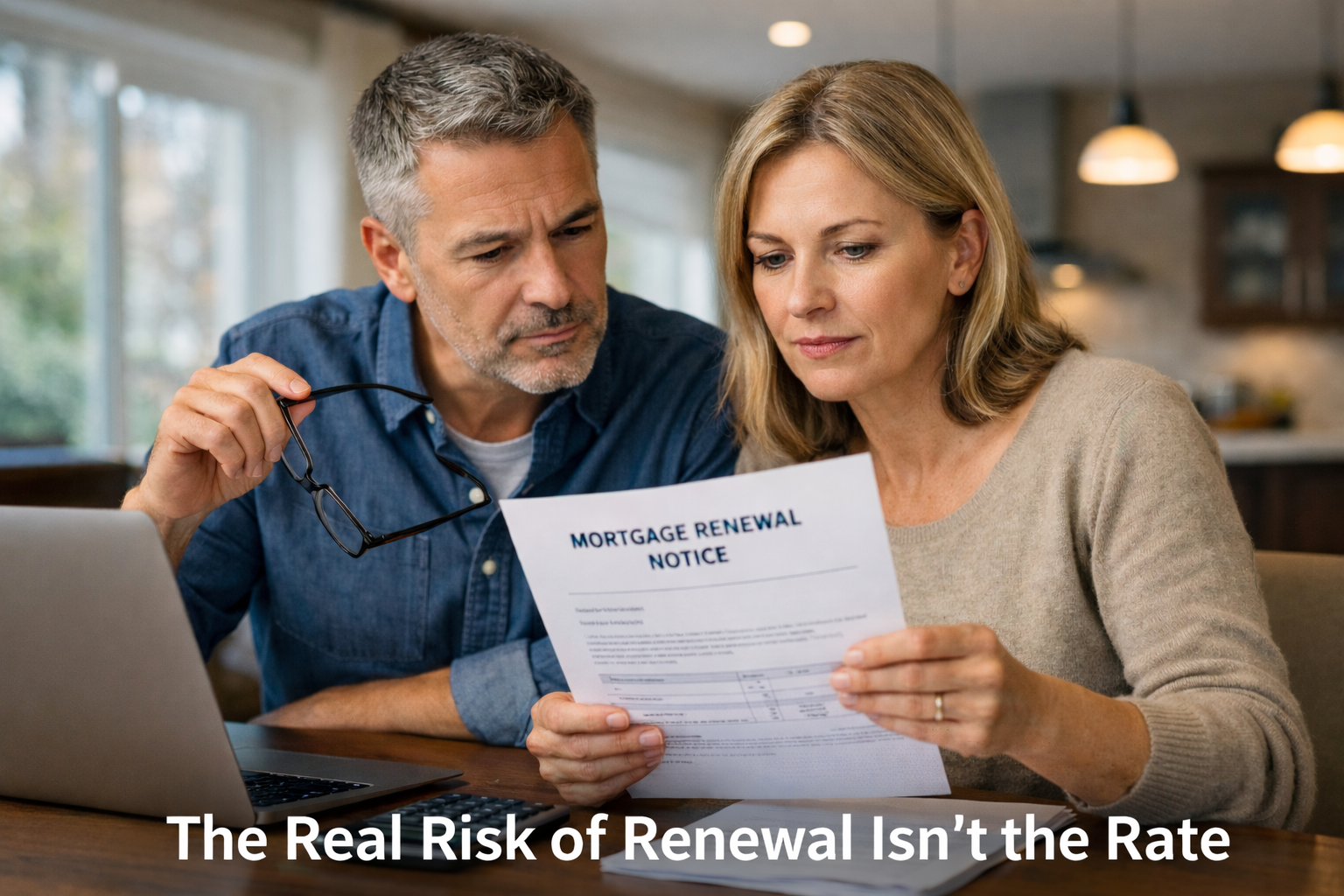

If you're in a mortgage that qualifies for renewal in the next few months and you must have considered staying with the current lender, you are not alone. The Canadian Mortgage and Housing Corporation's (CMHC) Residential Mortgage Industry Report of 2018 stated that mortgage renewals with the same lender have increased nearly 16% since 2017.

Furthermore, the report suggested that tighter approval criteria are a significant factor contributing to this increase in borrowers renewing their mortgage with the same institution. Late in 2017, the Office of Superintendent of Financial Institutions (OSFI), which regulates the financial industry, announced tighter rules on mortgage approvals. Therefore, consumers are worried that they may have trouble qualifying if they use a lender not acquainted with their history.

However, tighter mortgage rules did not affect the approval rate for same lender renewals. The CMCH reported a stable 99% acceptance rate. The report also noted that these renewals are not impacted explicitly by the new stress tests and, therefore, more likely to meet the current lender criterion.

Nonetheless, there is good reason to at least consider switching lenders once your mortgage's tenure is over. Get in touch with a professional such as a mortgage broker or agent to access good market knowledge.

On that note, remember that most lenders will send you a Letter of Renewal between three and six months before your term expires. Usually, the lender will offer you a new rate at that time, and you have to sign the document/letter and send it back to roll over the mortgage. That's all there is to it.

Unfortunately, lenders will often offer a higher rate to an existing customer than a new client because they're banking on the ease of renewal outweighing the higher rate. But at this point, you should ask yourself, "is it truly worth the time and effort it will take to switch? Will the few basis points shaved off off the rate or a few hundred dollars over a term worth making the switch?"

For most people, the answer will remain "no". However, the more significant your mortgage, the more enormous impact a small change can have. A few basis points off your rate could save thousands of dollars which is definitely something to consider no matter how rich you are. While everyone's situation is different, the more considerable the mortgage, the more significant the savings will be when you find a lower rate.

Using a different point of view, many first-time homeowners tend to use the same institution their parents used because they didn't know any better. Instead of falling into that trap and living with something you are not pleased with, you could switch to a different lender as the mortgage comes up for renewal.

In any case, a mortgage broker can significantly help you make a better decision.

Contact me today if your mortgage is coming up for renewal.

Rodney Schunker | Mortgage Broker (Lic. M12000165)

Cell: 416-697-6423 | Toll Free: 1-855-787-7723

Fax: 1-855-787-7723 | Web: www.kingdommortgages.ca

Mail: 10 George St North, Suite 202, Brampton L6X 1R2

Email: schunkerr@gmail.com

Rock Capital Investments Inc. Brokerage #10556. Each office is independently owned and operated. Proud member of Mortgage Centre Canada.